For most of recorded history, the largest economy on Earth was China's.

Not by a hair, and not briefly: for roughly eighteen of the last twenty centuries China sat at or near the top — printing books and spending paper money while medieval Europe still counted wealth in livestock. Then, in a single brutal century, it fell to the bottom, among the poorest places alive. Which is why rise is the wrong word. China is not rising — it is returning, clawing back to a rank it considers normal, and that is what lends the effort its ferocity.

China built a machine — market incentives bolted onto an unusually capable party-state, financed by a quiet tax on its own savers — and aimed it at a single target: catch the rich world. It worked better than any growth engine in history, lifting some 800 million people out of poverty in a generation. But the very same machine is now manufacturing the crises: the property bust, the mountain of hidden debt, the demographic cliff.

Which leaves the question that decides everything: can China get rich before it gets old?

To weigh it, two others ride alongside: India, the giant that began just as poor, and the United States, the frontier everyone is chasing.

Part 0 — The fall

The fall is the part outsiders forget.

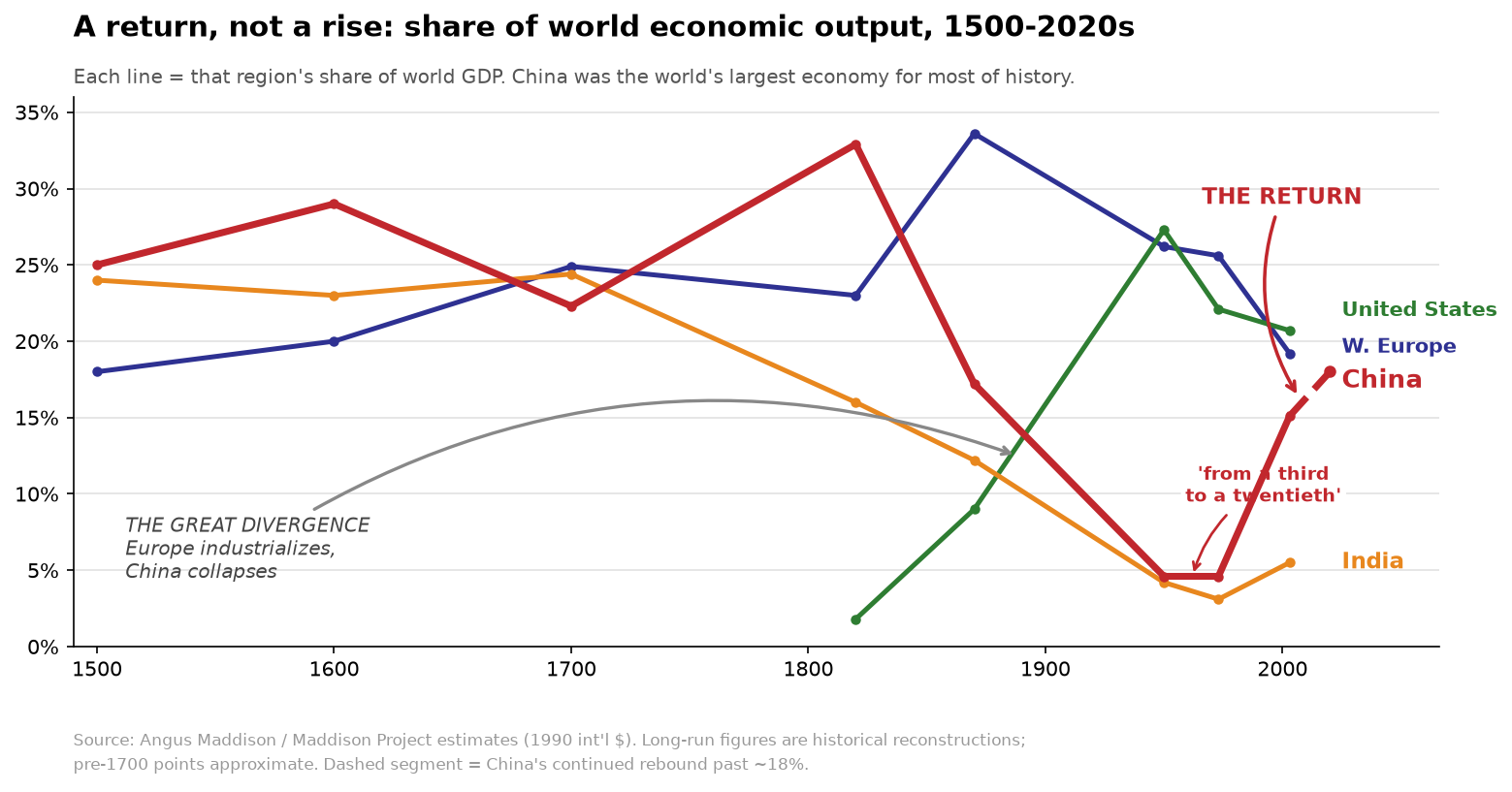

For roughly a thousand years the center of economic gravity sat in the East. Song-dynasty China (960–1279) ran what one historian named a "medieval economic revolution": the world's first paper money, iron output Europe wouldn't match for centuries, teeming commercial cities, and the four inventions that would remake everything — paper, printing, gunpowder, and the compass. As late as 1820, on Angus Maddison's much-cited historical reconstructions, China by itself produced something close to a third of world output.

Then the West industrialized and China didn't — the reversal economic historians call the Great Divergence (the term comes from Kenneth Pomeranz's 2000 book). Coal, steam, and the factory multiplied European output per person; China's stagnated and then sank. In Maddison's blunt phrase, China's share of the world economy fell "from a third to one twentieth" between 1820 and 1952. Chinese output per person shrank while the West's quadrupled.

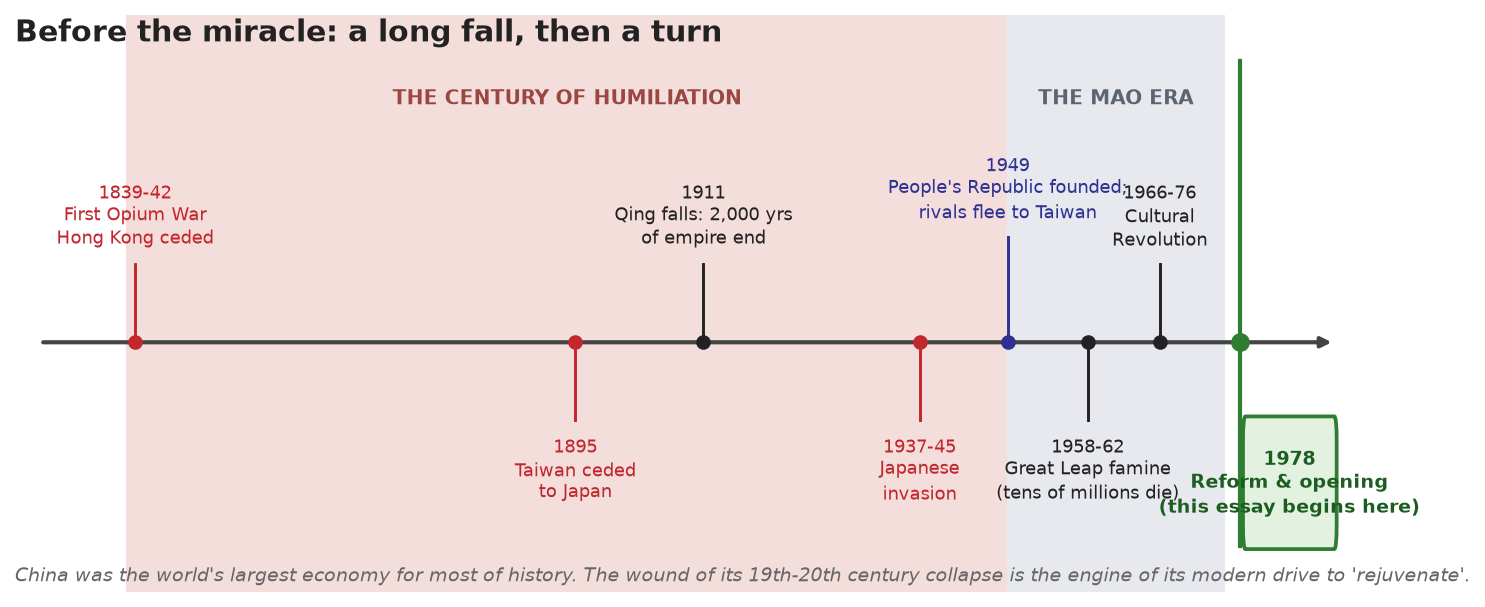

The hundred years China never forgot

The collapse was a national trauma, and the Chinese state has a precise name for it.

It is called the Century of Humiliation, running from the First Opium War (1839) to the founding of the People's Republic (1949). When the Qing empire tried to stop British traders from selling addictive opium into China, Britain won the resulting war and dictated the first of the "unequal treaties" — taking Hong Kong and exempting foreigners from Chinese law. The wounds compounded: a second Opium War; the Taiping civil war that killed perhaps twenty to thirty million; defeat by a modernizing Japan in 1895 and the loss of Taiwan; the 1911 fall of the Qing, ending two thousand years of imperial rule; warlord fragmentation; and the Japanese invasion of 1937–45, which killed an estimated fourteen to twenty million Chinese.

It is the emotional core of modern Chinese politics. The Party teaches the humiliation in every classroom and reaches for it constantly, and Xi Jinping's signature phrase — the "Chinese Dream" of "national rejuvenation" — is an explicit vow to reverse it. When China spends fortunes chasing self-sufficiency in computer chips, or refuses any compromise over Taiwan, the century is the reason.

Mao's deadly detour

The humiliation ended in 1949. After decades of civil war, Mao Zedong's Communists won and proclaimed the People's Republic, driving the defeated Nationalists across the strait to Taiwan — and planting the dispute that smolders there to this day. Yet the new regime spent its first three decades proving that a determined state pointed the wrong way can be as deadly as any foreign army. Mao's Great Leap Forward (1958–62), a forced crash-industrialization, caused the worst famine in recorded history — estimates run from fifteen to fifty-five million dead, most clustering above thirty million. The Cultural Revolution (1966–76) then turned the country on itself, as Mao loosed student militias to purge his rivals and shatter the institutions of the state.

When Mao died in 1976, China was exhausted and poor. Two years later Deng Xiaoping rose at a Party meeting and, without ever uttering the word, pointed the country toward capitalism. A nation that had tried utopian planning and buried tens of millions chose, instead, to get rich. Everything that follows flows from that turn.

The Party that never let go

What the turn did not change was who held power. The organization that won the civil war — the Chinese Communist Party, founded in 1921 — has never loosened its grip, and the growth story makes no sense without it. The CCP is not a political party in the Western sense; no rival could win an election. It is the load-bearing spine of the whole state: government, courts, and army all answer to it — "the Party commands the gun" — and at every level the Party secretary outranks the mayor or governor. With more than 100 million members, it is among the largest organizations in human history.

Two facts about it surprise outsiders. Despite the name, today's China is mostly capitalist — by the government's own accounting, private firms generate roughly 60% of GDP and 80% of urban jobs. And the Party's claim to rule rests not on votes but on delivery — prosperity, order, and national strength traded for a monopoly on power, a logic scholars call performance legitimacy. That bargain is the hinge of everything ahead: the growth machine is not merely economic policy but the regime's survival strategy, pursued with a ferocity no electoral government could match. The Party steers through technocratic tools — Five-Year Plans since 1953, promotions handed to officials who hit their growth targets — and in 2018 Xi scrapped the term limit on the presidency, a turn back toward one-man rule.

Part 1 — The return

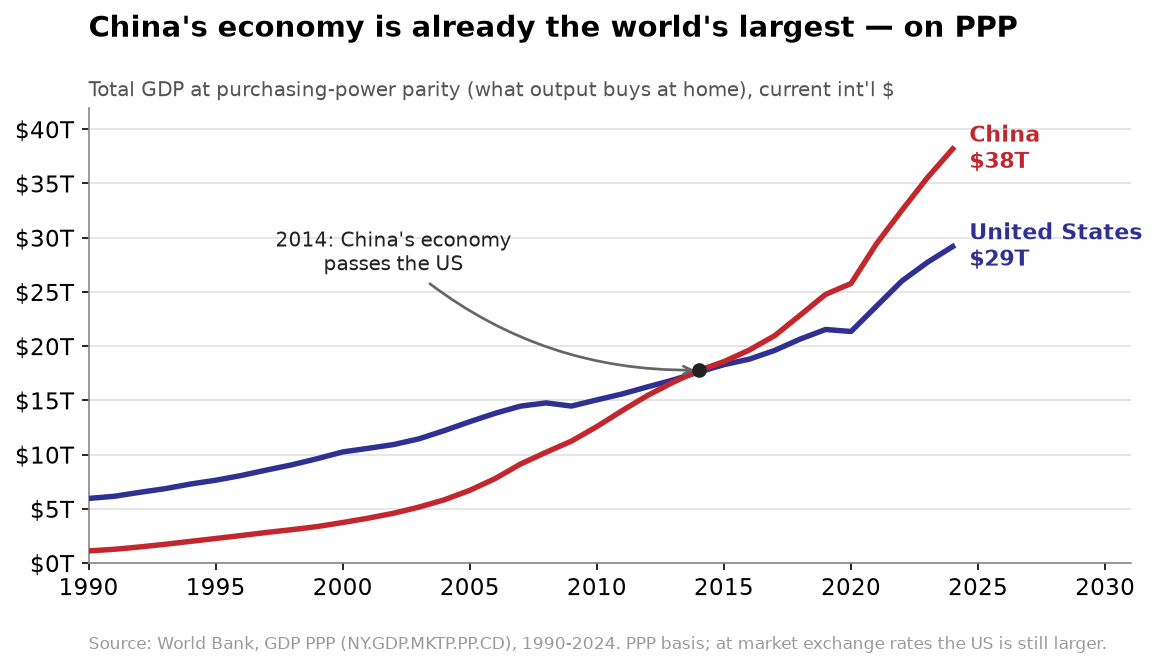

In 1978, on the eve of reform, China was one of the poorest countries on earth — income per person was roughly a fortieth of the American level, below much of sub-Saharan Africa. Over the four decades that followed, real GDP grew by an average of about 9.5% a year, a pace that doubles an economy every eight years and holds it there for a generation. No large country had ever done this for so long. China passed Japan to become the world's second-largest economy in 2010, and on a purchasing-power basis — what incomes buy at home — it overtook the United States around 2014. Measured that way, China's is already the largest economy on Earth.

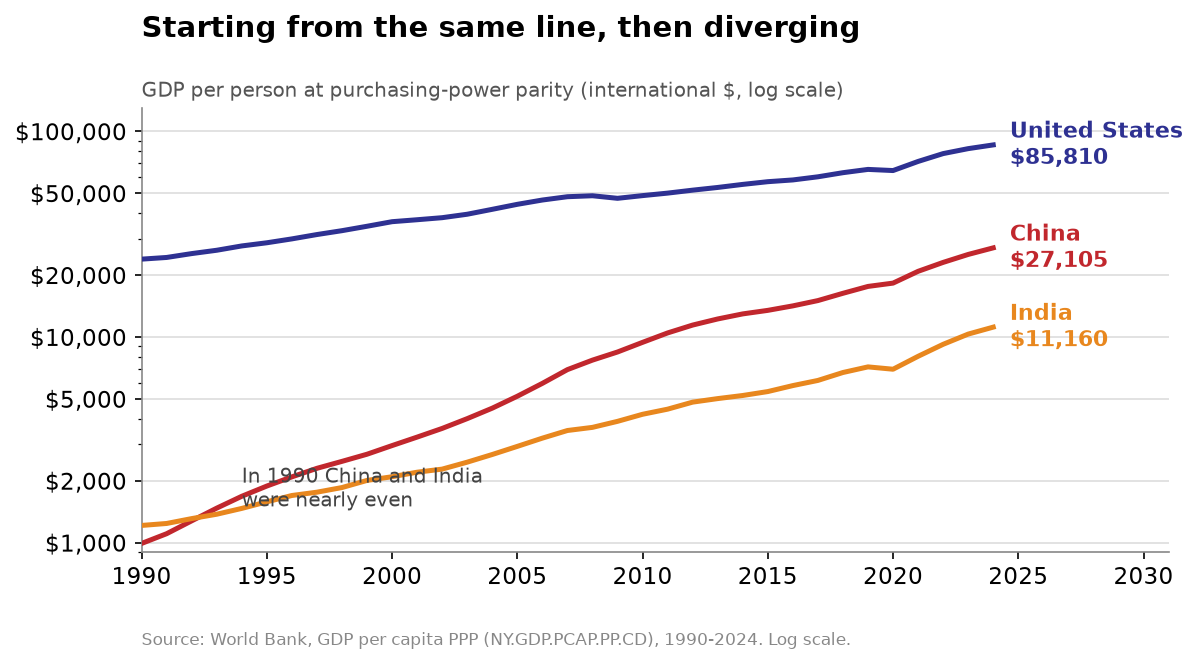

That is total size. Per person the picture inverts: China is still far poorer than the United States — and the sharpest comparison is with India.

In 1980 the average Chinese and the average Indian were about equally poor — a few hundred dollars a year each. As late as 1990, India was still the richer of the two per person. Then the paths forked. Over the following decades India grew respectably, at about 6% a year; the mature American economy grew at about 2.7%. China grew at 9.5% — and compounded across a generation, those three rates open into canyons. By 2024 the average Chinese citizen produced around $27,000 a year at purchasing-power parity — roughly two and a half times the Indian figure, a recognizably middle-income life, though still under a third of the American $86,000. And notice the line that didn't move: the United States held about a quarter of world output in 1980 and about a quarter in 2024. America didn't shrink. China simply closed a gap that had been nearly the entire distance — its own share of world output climbing from under 2% to roughly 17%.

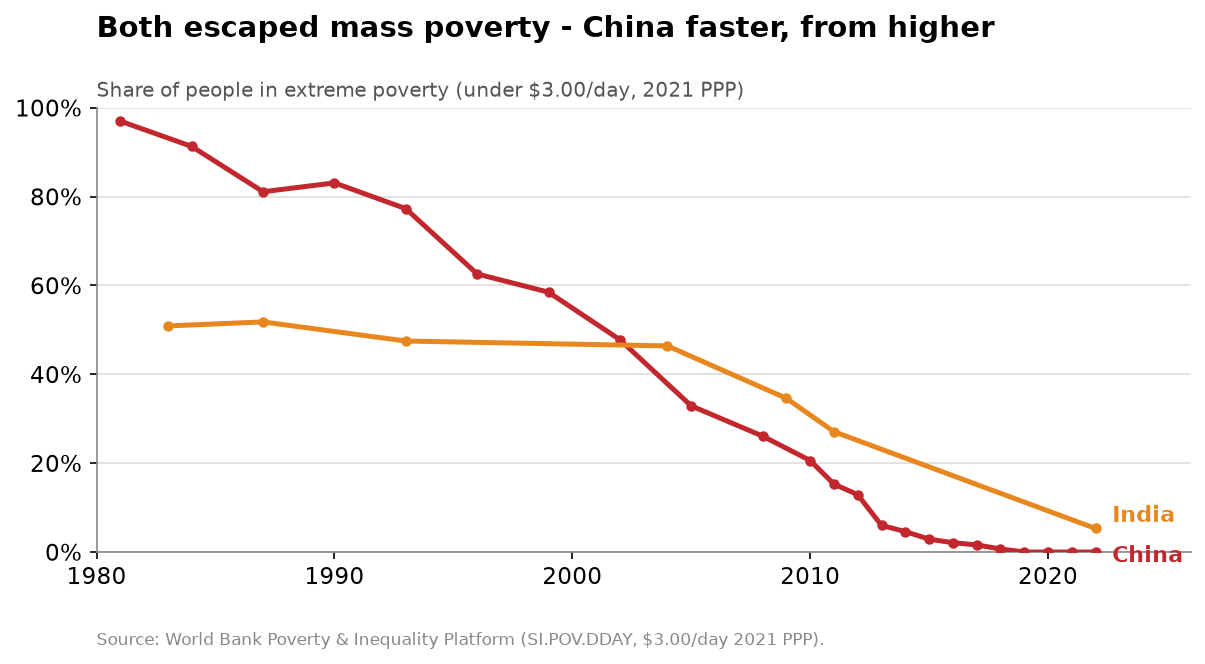

The most consequential number is human. By the World Bank's count, the number of Chinese living below the old extreme-poverty line of $1.90 a day fell by close to 800 million — a single country accounting for close to three-quarters of the entire planet's reduction in extreme poverty over that period. The asterisk comes in Part 3; the magnitude is real.

The physical scale is hard to hold in the mind. China now produces about 28% of the world's manufactured goods by value — more than the United States, Japan, and Germany combined. It built and runs the largest high-speed rail network on earth, roughly 48,000 km, about 70% of the global total, almost all of it since 2008. And the single statistic that best conveys the speed of construction: China poured more cement in the three years 2011–2013 than the United States used in the entire twentieth century.

The whole race, on one scorecard:

| Where they stood | China | India | United States |

|---|---|---|---|

| GDP per person (PPP), 1990 | ~$990 | ~$1,210 | ~$23,900 |

| GDP per person (PPP), 2024 | ~$27,100 | ~$11,200 | ~$85,800 |

| Avg. real growth, 1980–2019 | ~9.5%/yr | ~6.1%/yr | ~2.7%/yr |

| Life expectancy, 1980 → 2023 | 64 → 78 | 54 → 72 | 74 → 78 |

| Extreme poverty ($3/day) | 97% → ~0% | ~50% → 5% | ~0% throughout |

| Human Development Index, 1990 → 2023 | 0.50 → 0.80 | 0.45 → 0.69 | 0.86 → 0.92 |

In 1990 China and India were the same row of the same story — India a notch ahead, if anything. By 2024 China had moved up a class, India was still climbing, and the United States had barely budged from the top because it was already there.

One caveat: China's official statistics are not gospel — independent researchers argue some years' growth was overstated by local governments, so treat any single decimal with suspicion (the reliability question gets its own treatment in Appendix B). None of it overturns the broad story, though — the cement, the rail, the disappearance of mass hunger are visible from orbit.

Part 2 — The machine behind the miracle

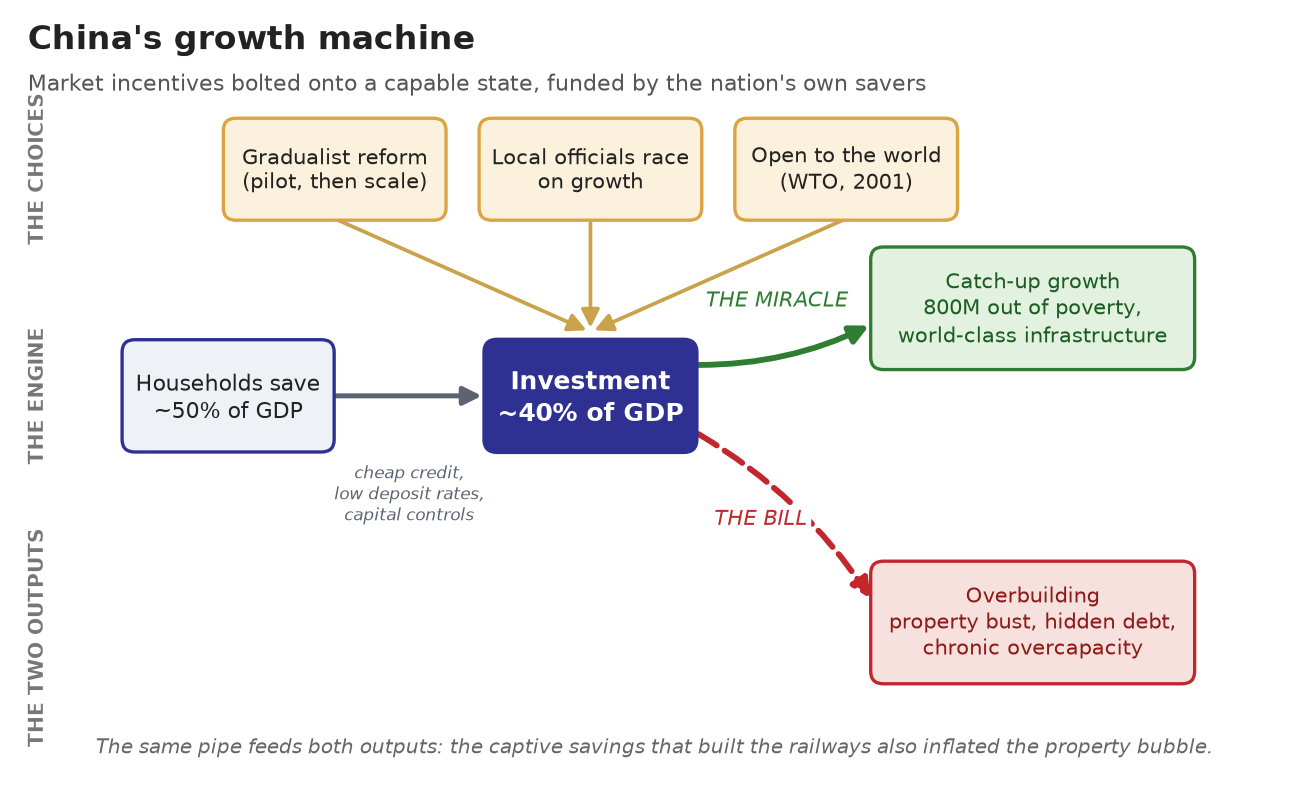

There was no single switch. What looks from the outside like one decision — China embraced markets — was a half-dozen distinct mechanisms bolted together over twenty years, each feeding the next: a way to free prices without creating losers; sealed-off zones to test capitalism in miniature; a bureaucracy rewired to chase growth; a banking system that quietly taxed savers to pay for all of it. They arrived roughly in that order, and that is the order in which they make sense.

i. Markets at the margin

China never freed everything at once. Rather than liberalize all prices and privatize all firms in a single stroke — the path the Soviet Union would soon take, to ruin — it changed the system at the edges and kept whatever worked. Deng Xiaoping's phrase was crossing the river by feeling the stones.

The device that made this survivable runs opposite to how most people picture markets arriving. A state factory still owed its quota at the old planned price — but now it could sell anything above the quota at whatever the market would bear. Overnight it had a reason to produce more and waste less, while nobody who depended on the old price lost a thing; there were no losers to revolt. Economists call it the dual-track price system, and the case that it was a rare "reform without losers" comes from Lau, Qian, and Roland. The counter-example was unfolding live next door: when Russia tried the all-at-once route — shock therapy — in the early 1990s, its output collapsed by roughly 40% and male life expectancy fell by years. China's gradualism, the historian Isabella Weber shows, was a deliberate choice, not an accident.

Capitalism itself was admitted the same careful way — through walled gardens. In 1980 China fenced off four coastal Special Economic Zones, Shenzhen the famous one, where foreign firms got tax breaks and could import, assemble, and re-export freely. If the experiment failed, the wreckage stayed in one fishing district. It didn't fail: Shenzhen grew from a few hundred thousand people into a megacity of some 17 million, and the template was copied up the coast and inland.

ii. Officials as competitors

The mechanism outsiders grasp least may be the most powerful. China pushed real economic power down to local governments — then tied officials' careers to local growth. A leader who delivered was more likely to be promoted; one who lagged was passed over. The bureaucracy became a tournament: thousands of officials racing to pave roads, court investors, and clear ground for factories, because their own rise rode on the local GDP number. The early vehicle was the Township and Village Enterprise — the rural factory, collective in name and often private in fact — which multiplied from 1.65 million in 1984 to nearly 19 million by 1988, absorbing the surplus farm labor that decollectivization had freed. The same incentive had a shadow: it bred faked numbers and local protectionism, officials gaming the very metric that judged them — a pattern that recurs throughout this story.

iii. The capable state

Behind all of it sat a party-state with a capacity democracies struggle to match: it could mobilize resources, hold to a long-horizon plan, steer credit where it wanted, and build infrastructure at a speed that still startles visitors. Its hardest corporate reform even carried a blunt name — "grasping the large, letting go of the small": keep and fatten a few hundred strategic state firms as national champions, sell or shut the rest. The cost was savage and is often forgotten — tens of millions of state workers were laid off in the late-1990s restructuring — but the state came through able to aim capital and labor wherever it chose.

iv. The hidden tax

Now the least visible piece — the one that quietly paid for all the rest. Where did the money for that wall of investment come from? From Chinese households, through a mechanism almost invisible by design. China held bank deposit rates very low, at times below inflation, and used capital controls to stop savers moving money abroad. With nowhere else to put it, households kept saving in state banks — which lent it on, cheap, to state firms, exporters, and developers. Savers were, in effect, taxed to subsidize investment; Nicholas Lardy reckons the hidden levy ran to more than three times what the income tax collected. Economists call it financial repression, and it produced an investment rate the world had never seen at scale — national savings near 52% of GDP at the 2008 peak against a global norm around 20%, investment above 46% of GDP, all funded at home. Hold onto this one. It is the engine of the boom and the source of the debt now coming due: the same channel that financed real factories financed empty apartment towers.

v. Becoming the world's factory

Two outward moves finished the machine. In December 2001 China joined the World Trade Organization, locking in predictable access to rich-country markets and de-risking every foreign firm's decision to route its supply chain through China; exports grew thirteen-fold, from ~$250 billion in 2000 to $3.4 trillion in 2023 as the country became "the world's factory." Then, growing richer, the state shifted from enabling the economy to directing it — naming strategic sectors and pushing them with subsidies, cheap credit, and protected home markets under the banner Made in China 2025. It worked: China is now the global leader in 5 of 13 priority industries, and the showcase wins — electric vehicles, batteries, solar — now reshape world markets. But the subsidy machine that mints the wins also mints gluts: chronic overcapacity, ruinous price wars, unprofitable champions kept breathing by the state. Industrial policy here is neither clean success nor clean failure; it reliably produces both, at scale.

So: market, or state?

Scholars split over which half of the machine did the real work, and the answer is that the question is mis-posed. The mechanisms were never in tension as facts: China ran market liberalization and heavy state direction at once. The fight is about weighting — and the most persuasive resolution, the political scientist Yuen Yuen Ang's, refuses the binary. Markets and state institutions coevolved, she argues: the center set broad direction while local officials improvised wildly within it, so the credit belongs not to "the market" or "the state" but to the adaptive churn between them. (The fuller debate — the market-first and state-first camps, and where to read each — is in Appendix C.)

Either way, the spine holds: it was a machine with both kinds of parts, working only together. Here is the whole contraption on one page.

The boom and the reckoning run on the same plumbing. The cheap, captive savings that built the railways and the factories are the very same savings that inflated the property bubble and the debt. That is why the headwinds ahead are not a failure of the model so much as the model presenting its invoice.

Part 3 — Who gained, and what it cost

An average blends very different lives into one number. China's growth was real; the harder questions are how far it reached, how much daily life improved, how evenly the gains fell, and what they cost.

The poverty triumph — and its asterisk

The headline is true and astonishing. Against the international extreme-poverty line, the share of Chinese in extreme poverty fell from around 97% in 1981 to essentially zero by 2019. China then ran its own campaign to finish the job — Xi Jinping's "targeted poverty alleviation," which literally assigned officials to individual poor households — and declared total victory in 2021, 98.99 million rural people lifted since 2012.

India is the right yardstick here too. It also fought poverty and won ground — extreme poverty there fell from about half the population in the early 1980s to around 5% by 2022. But look at the shape of the two lines: China started higher — almost everyone was destitute in 1980 — and fell faster, crossing below India near the millennium and hitting the floor a decade ahead. Both giants escaped mass poverty; one did it at a sprint.

The asterisk is a measurement point, not a gotcha: "poverty" has no single line. China's own national line sits near $2.25 a day — a poor country's standard, close to the World Bank's extreme threshold — and by it, poverty is gone. But by the Bank's line for upper-middle-income countries like China, $6.85 a day, 21.3% — roughly 300 million people — were still poor in 2022. Both are true at once: extreme poverty in China is over; broader poverty is not. (The full ladder of poverty lines, and a much-abused statistic to handle with care, is in Appendix B.)

Life, remade

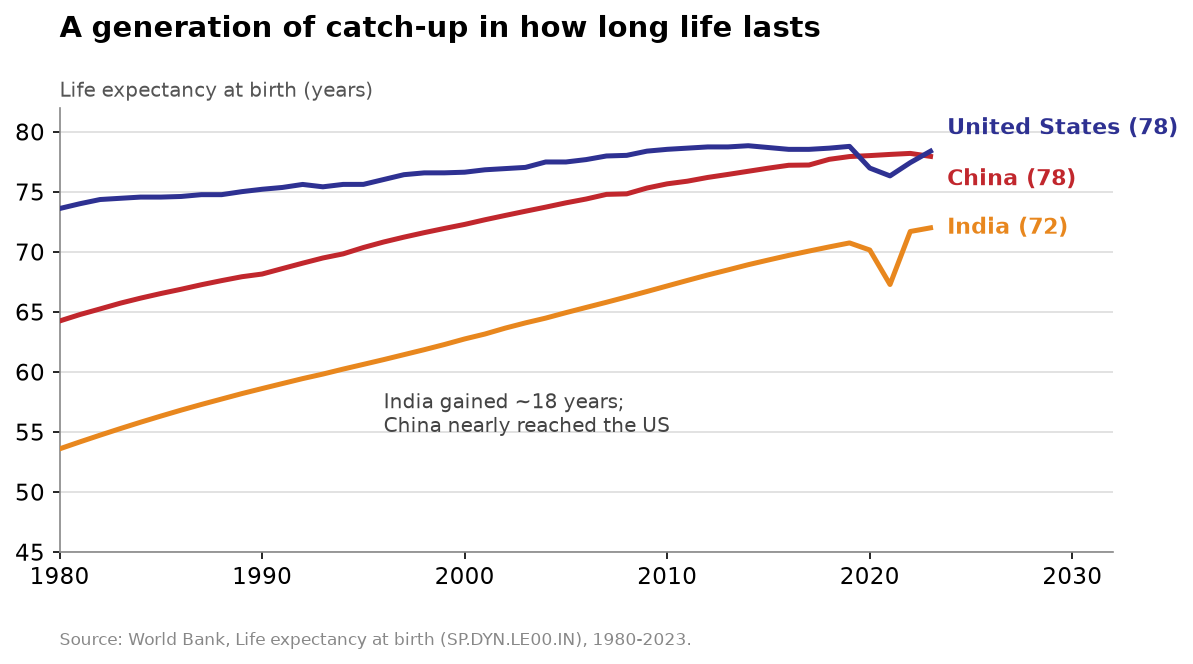

Whatever one thinks of the politics, the lived improvement for ordinary Chinese over a single generation was among the largest in recorded history. Start with how long life lasts: life expectancy rose from about 64 years in 1980 to roughly 78 in 2023 — a fourteen-year gain in four decades that the rich world took a century to make.

The catch-up is vivid on a single axis. In 1980 an American outlived a Chinese citizen by a decade and an Indian by twenty years; by 2023 China had pulled nearly level with the United States, 78 to 78 — startling for a country a third as rich — while India still trailed at 72. China is the only country ever to climb from the UN's "low" human-development tier to its "high" one, starting neck-and-neck with India in 1990 and ending a full class ahead. Daily life was remade to match: near-universal literacy and over 60% of young people in higher education in a country illiterate within living memory; near-universal electricity; the world's largest high-speed-rail and metro networks; and a leap clean over credit cards into a cashless economy where a billion people pay by phone.

But the gains tilted

China entered the reform era one of the more equal societies on earth — a legacy of collectivism — and the boom pulled it sharply apart. The official Gini coefficient (0 = everyone equal, 1 = one person owns everything) climbed from about 0.31 in 1981 to a 2008 peak of 0.49 and has held near 0.47 since — more unequal than Western Europe, roughly US-level — and independent estimates that fold in tax records put the top tenth's income share at 41%, the bottom half's at 15%.

The deepest divide runs between city and countryside, and one institution hardened it into something close to a caste line: the household registration, or hukou. Every citizen is registered rural or urban, and that label — not where you live or work — governs access to schools, hospitals, and subsidized housing. A man can pour concrete in Shanghai for twenty years and his children still be barred from its public high schools. The trap created a floating population of roughly 290 million migrant workers — the people who physically built the boom, living as second-class residents in the cities they built. Reforms are loosening it (over 40 million gained urban status in 2021–2023), though the biggest cities stay hardest to enter. Where you're born compounds it: the richest province out-earns the poorest four to one — a between-countries gap, inside one country.

By 2021, with a billionaire class rivaling America's, inequality had become a political problem, and Xi answered with a Common Prosperity campaign — redistribution rhetoric, a crackdown on "obscene" wealth, a ban on for-profit tutoring. Then the property crisis hit and it quietly softened: when growth and equality collided, growth still won.

The costs

The gains carried costs the people who lived through them felt keenly. The most visible was the air: at the 2013 Beijing "airpocalypse," fine-particulate pollution ran many times the WHO's safe level. Then it reversed — after a 2014 "war on pollution," national particulates fell by more than 40%, with China alone driving most of the world's air-quality gain of those years — even as the country stays both the largest carbon emitter and the largest deployer of clean energy, a paradox to hold rather than resolve. Other costs were human: the punishing "996" culture of 9-to-9, six days a week, ruled illegal in 2021 yet still common; trust failures like the 2008 melamine-milk scandal that harmed 300,000 infants. And corruption ran through all of it — less petty bribery than elite "access money" that greased the deals and deferred a systemic bill (Appendix D). Against them, a safety net that barely existed in 1980 now reaches far: basic medical insurance covers about 95% of the population.

Part 4 — The machine's bill comes due

Here certainty ends and judgment begins. The headwinds below are not forecasts — they are already happening. Where they lead is a matter of opinion.

Three headwinds already here

Demographics have turned — the deepest and least reversible. China's population has fallen for four straight years, with just 7.92 million births in 2025, less than half the 2016 figure; the fertility rate, around 1.0 child per woman, is among the lowest on earth, and the over-60s are now 23% of the country. The one-child policy (1980–2015) did its work too well, and the pro-natal turn has done nothing to reverse it. The demographic dividend has become a demographic debt.

The property engine has seized. Real estate swelled to a quarter to a third of the economy — a dangerous concentration. When Beijing moved in 2020 to deflate the bubble, the giant developer Evergrande defaulted on over $300 billion and others followed; home prices have fallen for more than two years. Because housing was the main store of household wealth, this is a hit to the savings of the whole middle class.

Hidden debt is coming due. The financial-repression engine has a back end: local governments borrowed through off-the-books vehicles to fund the building, meaning to repay from land sales — and the developers have stopped buying land. Official-plus-hidden local debt hit about 84% of GDP in 2024, up from 62% in 2019; total economy-wide debt is near 300% of GDP. A ~$1.4 trillion rescue in late 2024 buys time rather than a fix.

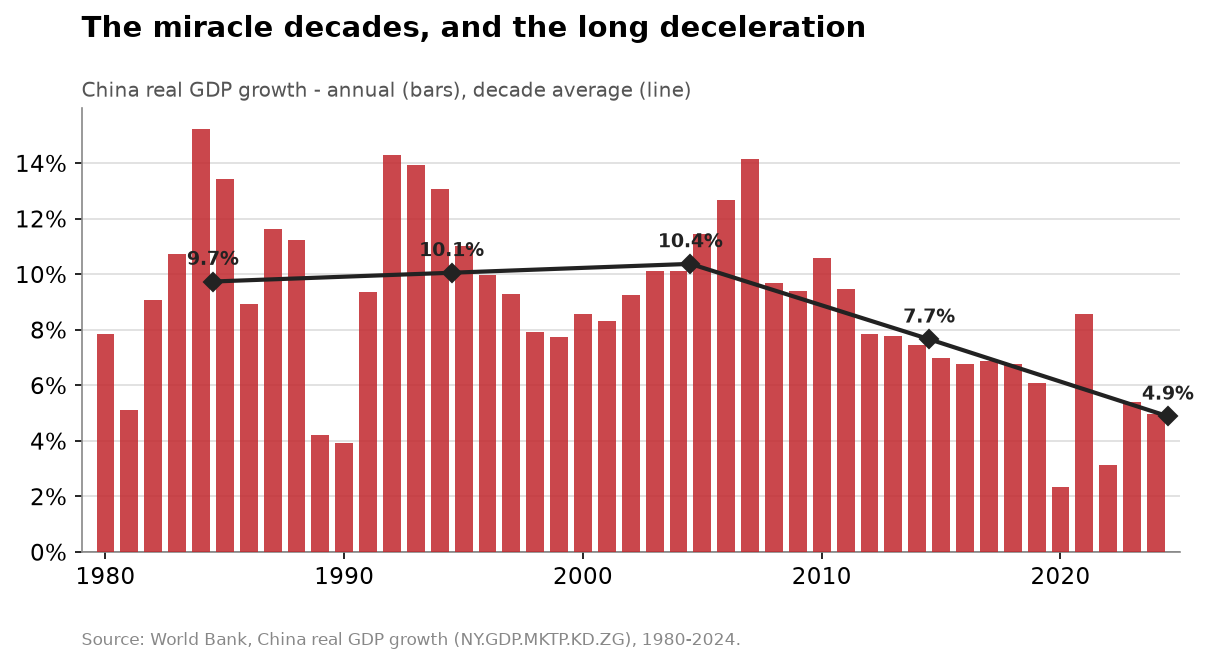

The cumulative effect is a long slowdown — inevitable (no economy compounds at 10% forever) but steeper than the leadership would like.

The decade averages tell it cleanly: ~10% a year through the 1980s–2000s, then a step down to under 8% in the 2010s and under 5% in the 2020s. Even the official ~5% target is contested — the independent Rhodium Group puts actual 2025 growth below 3%. The gap between official and independent figures is itself the finding; don't average it away.

The new engine

Against the headwinds sits something real: China is swapping its growth engine — out with property and construction, in with advanced manufacturing — and on the "new three" it already leads the world. It makes around 70% of electric cars (BYD passed Tesla as the biggest EV seller in 2025; EVs were 41% of its new-car sales in 2024) and controls over 80% of the solar supply chain, with clean energy reaching ~10% of GDP. The catch is familiar: the same subsidy machine breeds gluts, and the surplus pours into a world raising tariff walls. The pivot is real, but it adds output more slowly than property is subtracting it.

Taiwan: the one thing it can't make

One gap hangs over all of it, and it leads back to the island we left in 1949. The thing the modern economy can least do without is the advanced computer chip — the brain of every phone, data center, and AI model — and its supply has a single point of failure: one company, Taiwan's TSMC, makes the large majority of the world's most advanced logic chips, on a self-governing island Beijing claims as its own. China has spent fortunes to close the gap — despite US export controls since 2022 it engineered a partial resurgence — but remains several nodes behind. That makes Taiwan the single largest unbounded risk in the story: the unfinished business of the civil war and the emotional summit of "rejuvenation," and a load-bearing joint in everyone's supply chain. A serious conflict there would sever the global economy at its most fragile point — which is why no forecast below can price it in. (Appendix E goes deeper on the chip war.)

Three ways it could go

Where does it go? Three serious views, each opinion, because nobody knows.

- The bull case (economists like Nicholas Lardy): with the right policies — above all, finally letting households consume more — China still grows respectably and becomes the advanced-manufacturing superpower of the coming decades.

- The bear case (Nouriel Roubini and others): a burst bubble, crushing debt, rapid aging, and a turn back to state control add up to Japan-style "lost decades."

- The muddle-through (Michael Pettis, the IMF's baseline): no collapse, no revival, a long deceleration toward ~3.5% by 2030, with the postponed work being to shift from investment to consumption.

The question beneath all three is whether China gets rich before it gets old — whether the manufacturing pivot can outrun the demographic and debt drag. That is unknown, and anyone who tells you otherwise is selling a forecast as fact.

Coda — Rich before old?

Return to the frame we began with. For most of recorded history China was the largest economy on Earth; for one buried century it was among the poorest; and what we lazily call its "rise" has been the long climb back. The climb was powered by a machine — market incentives bolted onto a capable state, funded quietly by its own savers, aimed with single-minded force at catching the rich world. It worked better than any growth engine in history. It also, like every machine, threw off waste heat, and the waste is now the story. The property bubble was built by the financial-repression engine. The mountain of local debt was the price of the build-everything tournament. The demographic cliff is the long echo of the one-child policy. The headwinds aren't a betrayal of the model; they are the model, presenting its invoice.

What's uncertain isn't whether China grew — it did, beyond dispute — or even whether the gains were shared, which they were, unevenly and incompletely. It's a subtler question: whether a system this good at directing an economy toward catch-up growth can re-tool itself for the harder job of running a rich, aging, consumer society — where the right move is more often to let go than to build, and where you can't promote your way out of a low birth rate. China spent forty years proving it could do the hard thing that has a blueprint. The next forty will test whether it can do the harder thing that doesn't.

Appendix AQuestions for the table

-

The tournament. China tied officials' careers to local growth, and they built like men possessed. Could a democracy wire up that incentive — or does it need a world without voters? Would you want your mayor judged that way?

-

Freedom, priced. Would you trade open elections, a free press, and the right to mock the powerful for China's last forty years of material gain? Now answer again, not knowing which family, province, or hukou you'd be born into.

-

Floor versus gap. China raised the floor and let the gap explode; India kept the gap smaller, from a lower floor. Born at random into one in 1980 — which? And what does the choice say about what you actually value?

-

The motive. If a nation's deepest drive is to avenge a humiliation and restore a lost greatness, how will it behave once it finally arrives?

-

What does the experiment prove? Two equally poor giants, one autocratic, one democratic — and China ran away with it. Does that prove anything about autocracy, or are there too many other variables to say? Would you tell a poor country to copy the playbook?

-

The machine's dilemma. The same engine built the miracle and the crises. Run China tomorrow: dismantle it for slower growth, or keep feeding it toward the bust — when no move is both safe and enough? And can a government fix a birth rate, or is that just what wealth does?

-

Rise, or correction? China topped the world economy for eighteen of the last twenty centuries. So which is the anomaly — Western dominance, or everything before it? And if this is a return to the mean, not a rise, how should the West rethink "competing"?

-

Market or state? The boom ran on private incentive and heavy state control. Pick the one that did the real work — then argue the other side as hard as you can. Where does your view crack?

Appendix BHow much can you trust these numbers?

Four sources behind this essay deserve a skeptic's note.

China's official GDP. Beijing's headline numbers are not gospel. Researchers using satellite night-lights and other proxies argue that growth in some years was overstated by local governments; the economist Chang-Tai Hsieh frames the distortion less as central fabrication than as errors the national statistics bureau cannot fully control. The direction of the bias is itself disputed. The physical record — cement, rail, the end of mass hunger — is not, which is why the broad story survives heavy discounting of any single decimal.

The poverty ladder. "Extreme poverty is gone" and "300 million are still poor" are both true because they use different lines:

| Poverty line (purpose) | China, early 1980s | China, recent |

|---|---|---|

| $2.15/day (extreme) | ~97% (1981) | ~0% (2019 on) |

| $3.65/day (lower-middle income) | ~99.7% (1981) | 0.5% (2022) |

| $6.85/day (upper-middle income) | ~100% | 21.3% (2022) |

A statistic to handle with care: the economist Indermit Gill's line that "80 to 90% of Chinese would be considered poor" is measured against the American poverty line (~$21.70/day) — a bar that would classify much of the world as poor. It is not the international $6.85 figure, and conflating the two is the most common error in this debate.

The deep-history shares. The "a third of world GDP, then a twentieth" figures and the long-run chart in Part 0 come from Angus Maddison's historical reconstructions — scholarly estimates built from sparse data, not measured accounts. Editions disagree, and pre-1700 points are approximate. They carry the shape of the story (dominance → collapse → return), not any exact percentage.

The disputed tolls and the chip share. The Great Leap famine toll (15–55 million; most estimates above 30 million), the Taiping toll (~20–30 million), and China's WWII dead (14–20 million) are ranges, not counts. And "~90% of advanced chips" holds only for leading-edge logic — China and others make plenty of older and memory chips; the chokepoint is the cutting edge alone.

Appendix CThe state-vs-market debate, and where to read more

How much of the miracle was the market, and how much the state? The scholarship splits three ways, and which way you lean decides what you think China should do next.

- Market-first — Yasheng Huang, Capitalism with Chinese Characteristics: the 1980s takeoff was bottom-up, powered by rural private entrepreneurs; welfare gains weakened once the state reasserted itself in the 1990s. China grew fastest when the state stepped back.

- State-first — Justin Yifu Lin, New Structural Economics: an active, capable government — picking sectors, building infrastructure, steering credit — was indispensable, and today's EV-solar-battery dominance is the proof.

- Coevolution — Yuen Yuen Ang, How China Escaped the Poverty Trap, the view this essay takes: the question is mis-posed. Market and state grew up together through "directed improvisation" — the center setting direction, local officials improvising within it.

Further reading: Isabella Weber, How China Escaped Shock Therapy (the reform-versus-shock-therapy choice China faced in the 1980s); and Barry Naughton, The Chinese Economy: Adaptation and Growth (the standard one-volume history).

Appendix DCorruption: lubricant, drag, or deferred bill?

China's boom-era corruption was rarely the petty-bribe kind that throttles poor economies. The political scientist Yuen Yuen Ang (China's Gilded Age) calls the dominant form "access money" — elite exchange, where officials trade land, contracts, and regulatory favors for kickbacks and future advantage. Her unsettling claim: access money behaves like steroids — it can stimulate investment and growth in the short run while quietly building the systemic risk (debt, overcapacity, financial fragility) that comes due later. It pooled where the state controlled the most valuable assets: land finance, construction, state firms, banking, and local government — the same land-and-debt machine behind Part 4's headwinds.

Xi Jinping's anti-corruption campaign (2012–present) is the largest in Party history — by official tallies, more than 4 million cadres disciplined and roughly 500 senior "tigers" — and serves a dual purpose: genuine cleanup and the purging of rivals. Its documented side effect is bureaucratic risk-aversion — officials who stall and stop experimenting rather than risk a file. China's score on Transparency International's Corruption Perceptions Index has sat flat near 43 out of 100 (rank ~76 of 180) for years.

Lubricant, drag, or deferred bill? The answer is contested — Ang's "growth-coupled steroid" is the most-cited nuance; many economists still treat all corruption as net rent-extraction. Either way, it was a cost the boom carried, not one it escaped.

Appendix ETaiwan and the chip war

China's machine learned to make almost everything. It still cannot make the one input the rest of the modern economy runs on: the advanced logic chip. One company, on one contested island, makes nearly all of them — Taiwan's TSMC, over 90% of the world's leading-edge chips and roughly two-thirds of all foundry output. It is the tightest chokepoint in the global economy, and Beijing claims the island as its own.

The hopeful theory is that this very indispensability protects Taiwan — the "silicon shield": China will not bomb the fabs it depends on, and the West cannot afford to let them fall. The doubts run the other way. Indispensability can invite coercion as easily as deter it; a modern fab would stop working the day a war began, starved of foreign engineers, spare parts, and stable power; and America's own drive to copy the capability at home — TSMC's ~$165B Arizona build-out — is quietly thinning the shield it says it wants.

Washington's aim has been to lock China out of the cutting edge. The October 2022 export controls cut it off from advanced chips, AI accelerators, and the tools to make them; later rounds tightened the rules and pulled in the Netherlands and Japan, which is why ASML has never sold China the EUV lithography machine no cutting-edge fab can work without. China's answer was SMIC's 7nm chip inside Huawei's 2023 Mate 60 — a genuine feat, wrung from older tools without EUV — but it sits several nodes behind TSMC's 3nm, at low yields and high cost, and the frontier gap has not closed.

The cost of getting it wrong runs into the trillions: Rhodium puts well over $2 trillion of activity at risk in a blockade, Bloomberg Economics nearer $10 trillion — a tenth of world output — in the first year of a full war. If Taiwan's fabs went dark, the cutting edge of computing would go dark with them for years, with no second supplier to call.

Every factual claim above links to its source. Figures are current as of June 2026; the forward-looking section is explicitly a range of expert opinion, not a prediction. Where Chinese official statistics are the only source (GDP, demographics, poverty declarations), they're flagged as such — they are broadly corroborated by physical and independent evidence, but no single decimal should be taken as gospel.